When comparing funding options, many entrepreneurs in the U.S. naturally zero in on the interest rate. A lower APR is an obvious plus, but it’s not always the best measure. For rapidly growing businesses, such as start-ups, speed, flexibility, and even opportunity cost are frequently more important than APR. This is where business unsecured loans enter the equation, offering an alternative to traditional borrowing. Through this guide, we will move away from APRs and explore the actual cost implications of unsecured lending in comparison to secured loans so that you can determine when it is financially viable for you to pay a small premium in interest rates.

Why APR Alone Can Be Misleading

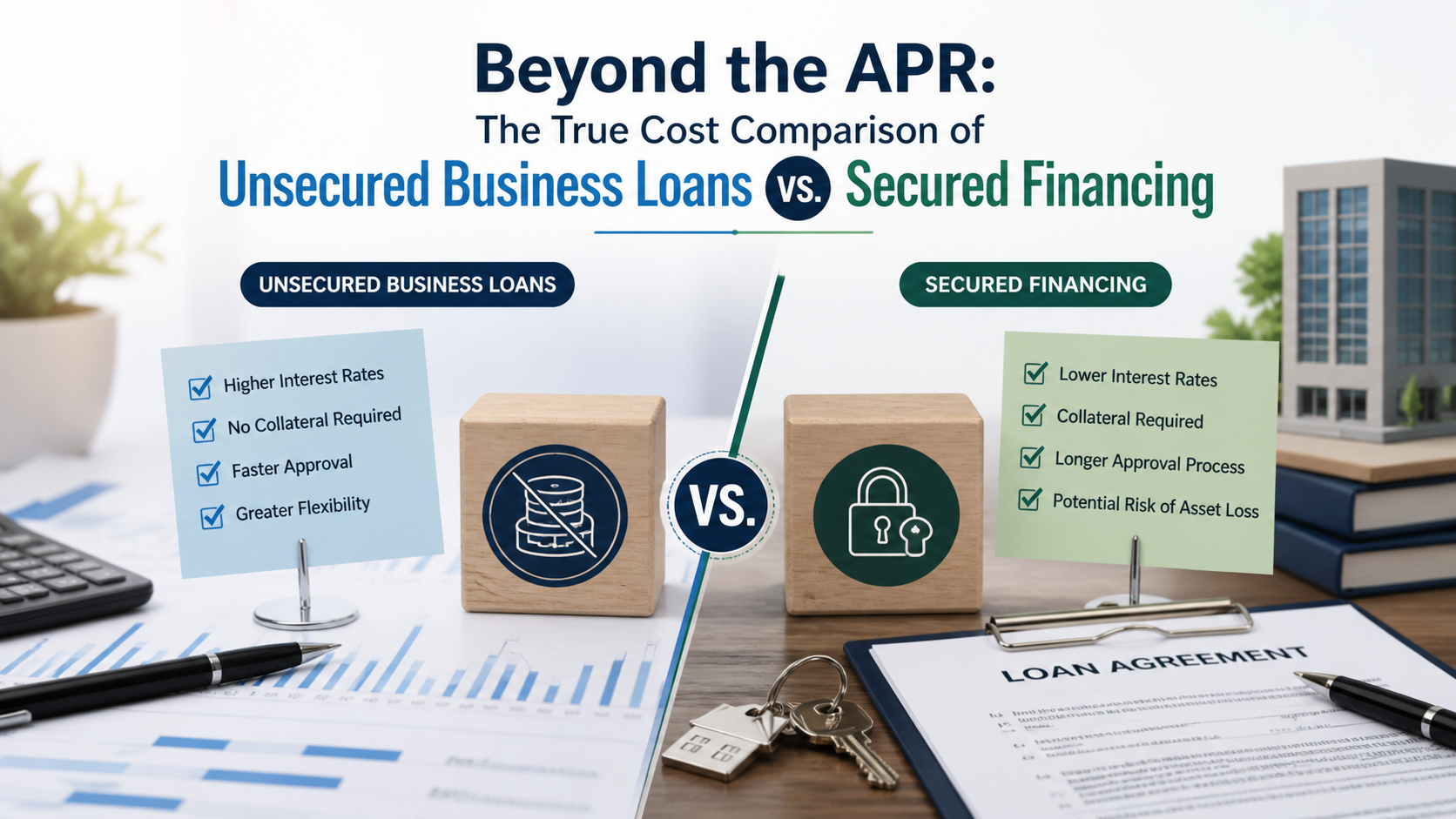

While the Annual Percentage Rate (APR) can be an attractive way to capture borrowing costs, it does not necessarily represent the operational effects on your organisation every day. For example, two loans could have very different APRs but have extremely different outcomes based on other factors associated with that loan, such as the length of time it took to be approved, the type of security offered as collateral, the amount of time required for administrative procedures, and so on.

In one case, it may take several weeks or even months for a secured loan with a lower interest rate to become available for use; however, a business unsecured loans could potentially allow you to access financing in as little as a few days. If you need financing to act quickly on a time-sensitive growth opportunity, the difference in funding access could outweigh any percentage point difference in interest rates.

Understanding Secured Financing

The loans that are backed by security require that you put up some form of collateral/property, such as real estate, machinery, or stock. Since the lender can take possession of the assets of the borrower, these loans usually come with:

- Lower interest rates

- Longer repayment terms

- Higher borrowing limits

Nevertheless, what is not so obvious is that the costs involved can be considerable. Property appraisals, legal opinions, and contracts consume both time and money. Most importantly, the pledged assets are exposed to risk. In case of a default, you may have to give up the property without which the business cannot function.

What Makes Unsecured Financing Different

Business unsecured loans are based on the cash flow and revenue patterns of the business. The interest rates may be high in the case of unsecured business loans; however, the benefits associated with them are usually underestimated in a cost comparison.

Benefits include:

- No collateral required

- Faster approval and funding

- Less paperwork required

- Less closing cost

- A flexible framework to support modern, asset-light businesses

In cases where businesses require agility, business unsecured loans would be a much better fit.

Evaluating Loan Options Accurately

To compare your small business loan near me options, you will want to include the total cost to you economically, not just the annual percentage rate, which is your interest rate.

- Funding Time: Many unsecured options allow you to be funded within 24 – 72 hours after you apply. With business unsecured loans, the speed of funding may allow you to capture opportunities for revenue that secured financing may miss.

- Opportunity Costs: If you have to wait several weeks for your loan’s approval, you may lose an opportunity for a contract or purchase inventory at a discount, or have to delay the launch of your new product.

- Risk Exposure: Secured borrowing means that you will put your core business assets as collateral. On the other hand, business unsecured loans limit your risk to cash flow.

All of these factors taken into consideration, business unsecured loans may ultimately be less expensive than secured loans even though unsecured loans appear to have higher nominal, or stated, rates.

Credit Quality and Pricing

Many people think that unsecured financing can only be given to risky borrowers. However, these days, a lot of lenders provide unsecured loans for good credit at very competitive terms, particularly for businesses that have stable revenue and a strong banking history. If the borrowers are qualified, business unsecured loans can be offered with reasonable interest rates, shorter terms, and predictable repayment schedules, all this without obtaining collateral.

Flexibility for Fast-Growing Companies

Today’s American companies, especially those engaged in e-commerce, SaaS, consulting, and professional services, may not require hard assets but instead produce high recurring revenues. For these companies, business unsecured loans are ideal since their financing structure aligns with their business model. In contrast to secured loans, the unsecured options are flexible in the sense that they do not limit future borrowings by tying down assets.

Conclusion

APR is a consideration, but not a determining one. The true cost of borrowing involves time, flexibility, risk, and missed opportunities. In fast-growing companies in the U.S., business unsecured loans offer strategic value that secured financing simply can’t match. It’s by analyzing the entire picture, not just the rate of growth, that you are able to select a method of finance that will promote growth rather than inhibit it.